A new report from the Institute for Fiscal Studies warns that England’s fragmented council tax support system is reducing incomes for the poorest households, weakening work incentives and increasing administrative burdens, and argues that integrating the benefit into Universal Credit could deliver clearer, fairer and more efficient support.

Council tax support provides means‑tested reductions in council tax bills for low‑income households. Since 2013–14, working‑age CTS has been fully localised in England, with councils responsible for designing and administering their own schemes. Scotland and Wales continue to run national schemes of consistent generosity.

While CTS is a relatively small component of overall welfare spending, for the poorest tenth of households it contributes an average of over £500 a year, equivalent to 6% of their income, making it a crucial part of the social safety net.

The IFS finds that English councils have cut the overall generosity of their working‑age CTS schemes by £630 million (14%) in real terms since localisation, largely driven by reductions in central government funding.

Meanwhile, Scotland and Wales have maintained more generous national schemes, whilst the poorest households in England have seen average disposable incomes fall by £106 per year (1%) as a result of CTS reductions. Alongside this, local policy changes have sometimes increased complexity, lacked clear rationale, and created inconsistencies between areas.

The IFS notes that while localisation allows schemes to reflect local priorities, it has also increased administrative burdens on councils and created confusing, uneven rules for claimants.

Because CTS operates separately from Universal Credit, many low‑income households face very high marginal tax rates when their earnings increase. This creates an effective marginal tax rate of 64%, and the IFS warns that in some cases it can be even higher.

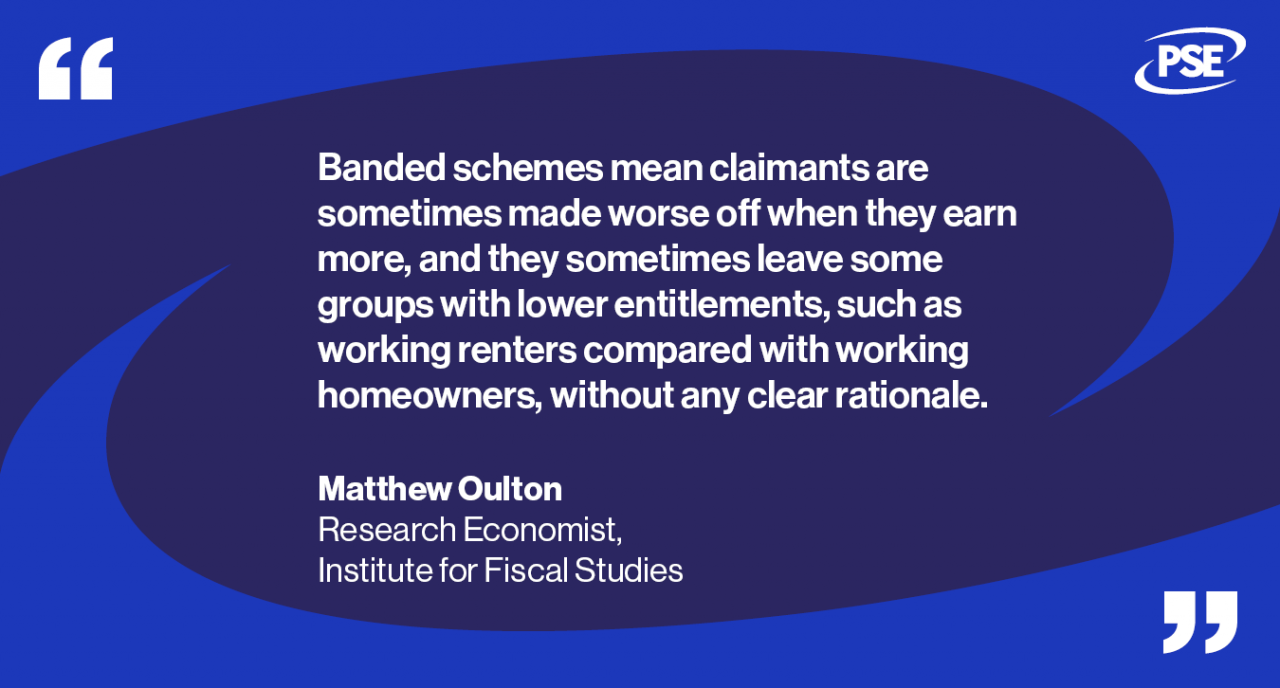

To simplify administration, many councils have introduced “banded schemes”, where CTS entitlement depends on falling within a particular earnings band. But this creates sharp cliff edges:

- A small increase in income can push a household into a new band, causing a sudden drop in support.

- Some working renters receive less support than identical working homeowners, due to quirks in how bands are defined.

The IFS argues there is often no clear policy reasoning behind these differences, which can penalise specific groups unfairly.

The IFS concludes that integrating working‑age CTS into UC would offer several advantages:

Benefits of integration

- Greater transparency for claimants

- Reduced administrative costs for councils

- A single taper, strengthening work incentives

- Clearer entitlement rules and fewer cliff edges

Challenges

- Strengthening work incentives could require either more spending, or reduced support for some poorer households

- Local autonomy would be reduced, though councils could still influence elements such as the share of council tax included in the UC calculation

The report emphasises that even if CTS remains separate, there is a strong case for avoiding banded schemes, suggesting more proportionate alternatives such as assessing income over longer periods.

Matthew Oulton, Research Economist at the IFS and author of the report, said:

“In devolving council tax support to local authorities in England, the government introduced local control over a part of the benefits system. But localisation has imposed a burden on councils to both design and administer a complex scheme. In many cases, local reforms seeking to ease administrative costs have, from the claimant’s perspective, added complexity to an already complicated system. Banded schemes mean claimants are sometimes made worse off when they earn more, and they sometimes leave some groups with lower entitlements, such as working renters compared with working homeowners, without any clear rationale.

“There is a strong case for integrating council tax support for working-age families into universal credit. This would not be without a downside: any form of integration could create some losers among both claimants and local authorities and could create risks for local authority finances if not handled correctly. However, integration would reduce complexity for claimants and administrative burdens for councils.”

With local government finances under continued strain and welfare complexity affecting millions of low‑income households, the IFS argues that reform of CTS should be placed firmly on the national policymaking agenda.

The report highlights that integrating CTS into UC could offer the most coherent route to a simpler, fairer and more efficient benefits system, one that is easier for households to navigate and more supportive of work.

Image credit: iStock